I spend a lot of my consulting hours sitting at conference tables in community-bank boardrooms, credit-union operations rooms, independent insurance broker offices, and RIA studies around Allen, DeKalb, Noble, Whitley, and Steuben counties. The conversation in 2026 has rotated. The question is no longer “should we be doing something with AI?” It is “we tried, and it stalled on data — what now?” Per the recent MIT Technology Review report on data readiness for agentic AI in financial services, that conversation is happening everywhere — not just in Northeast Indiana. The article cites Elastic's Global Managing Director of Search AI, Steve Mayzak, naming the dynamic directly: “Agentic AI amplifies the weakest link in the chain: data availability and quality.” The Forrester finding cited in the same article — that 57% of financial organizations are still developing capabilities to leverage agentic AI — is the national number behind the Fort Wayne conversation.

The fragment that makes the Fort Wayne version of the problem worse is structural. A typical NE Indiana community bank, credit union, or insurance brokerage runs on a stack assembled over twenty-plus years: a core banking ledger (FIS, Jack Henry, Fiserv, or a regional core), a separate KYC/AML platform, a fraud-monitoring overlay, a CRM the lending team uses but the deposit team does not, a customer-360 effort that was never completed, and a regulator-trace store the BSA officer maintains in a spreadsheet because the integration project got descoped twice. Layered on top of that is an unstructured-data estate — PDF disclosures, scanned KYC documents, advisor notes, claim narratives, loan files — that the MIT TR piece describes vividly: at one institution, Mayzak says, “60 different PDF types for the same content” had to be reconciled before an agent could answer one query. That is the Fort Wayne reality at a 250-employee bank with three branches. Agentic AI cannot run cleanly across that estate without a data-readiness audit first.

Key Takeaways

- The MIT Tech Review piece names the problem nationally: agentic AI amplifies fragmented financial data, and the majority of FS firms are not data-ready. The Fort Wayne translation is a six-question audit, not a vendor selection.

- NE Indiana community banks, credit unions, insurance brokers, and RIAs all run on a multi-decade stack of fragmented systems — core banking, KYC, AML, fraud, CRM, customer-360 — that no agent can navigate without a data-fabric layer.

- The architectural answer is the Secure AI Gateway, with PHI/PII redaction, regulator-trace store, and BSA/AML reportable-event logging server-side of the agent harness — never inside the agent.

- The regulatory stack — NIST AI RMF, FFIEC, OCC, Indiana DFI, Indiana AG, CSBS — defines the evidence requirements an FS agent has to satisfy before it touches production data.

- Four NE Indiana FS archetypes — community bank, credit union, insurance broker, RIA — each hit a different first data wall when they try to deploy their first agentic AI use case.

- The 6-week NE Indiana FS Data-Readiness Audit is the Cloud Radix engagement that produces a scored data-readiness baseline, a Gateway architecture sketch, and a prioritized 90-day remediation plan.

What does “data readiness” actually mean for agentic AI in financial services?

Most operators read “data readiness” as a clean-data problem. The MIT TR framing is sharper. Per Steve Mayzak in the MIT Technology Review piece, “It all starts with the data” — and the data problem has three legs, not one. The first leg is availability: can the agent reach the data at all, through what interface, with what authentication? The second leg is quality: is the data current, complete, deduplicated, normalized, and unambiguously described? The third leg is what regulators will care about most: auditability and explainability. Mayzak names it directly: “You need an auditable and governable way to explain what information the model found and the logic of why that data was right.” For an FS agentic deployment, that third leg is the one that determines whether the system can pass an exam.

The same piece names the determinism gap that bites every FS agent project. “There are many different ways to describe how to execute a trade at a bank,” Mayzak says. “In an agent-powered world, we need those descriptions to be deterministic.” For a NE Indiana community bank, the equivalent statement is that an agent reading the loan-decisioning workflow needs one canonical, deterministic description of how a loan moves from application to underwriting to decision — not the eight different oral histories that live in eight different officers' heads. The deterministic-description gap is where most FS agent pilots stall.

The Gartner data cited in the article — that more than half of financial services teams have implemented or plan to implement agentic AI — is consistent with what I am seeing in the field. Implementation intent is high. Production readiness is uneven. The gap between the two is the data-readiness layer, and it is the one Cloud Radix engagements spend the most time on in NE Indiana FS work.

Why is the FS data estate uniquely hard for agents?

Financial services has a data-estate shape that other regulated industries do not share. A NE Indiana hospital system has fewer, larger data systems (an EHR, an imaging archive, a revenue-cycle platform). An NE Indiana law firm has a relatively flat document-management system plus a billing platform. A community bank, by contrast, runs a stack that is both wider and deeper. The systems do not naturally talk to each other; the data definitions across the systems do not align; and the regulatory layer applies different evidence requirements to different domains within the same institution.

The result is that an agent built for “the bank” actually has to be five agents — or one agent with five carefully orchestrated data interfaces — covering the core ledger, KYC/AML, lending, fraud monitoring, and customer service. Each of those interfaces sits on a different data shape and a different regulatory regime. The data-stack-rebuilt-for-AI-agents post covered the broader architectural argument: legacy business databases were built for humans submitting queries, not for agents requesting deterministic, machine-consumable answers. The FS version of that argument is sharper because the regulatory cost of getting a query wrong is materially higher.

The fragmentation also creates a shadow-AI surface most FS operators underestimate. When the official data path does not exist, line-of-business staff find workarounds — copying customer data into a ChatGPT window to summarize, pasting loan narratives into a vendor portal to “speed up underwriting,” uploading PDFs to a public document-AI tool. The risk of that pattern in an FS context is severe; we documented the parallel mechanic in the Fort Wayne shadow AI data-leak playbook. For FS firms, the shadow-AI surface is not a remote possibility — it is the line-of-business reality if the official data interface is not built fast enough.

The 6-Question NE Indiana Financial Services Data-Readiness Audit

The audit is designed for a community bank, credit union, independent insurance brokerage, or RIA with $50M to $5B in assets — the institution-size band where most NE Indiana FS firms operate. Each question has a pass band, a partial band, and a fail band. Score honestly against your current state, not against what your three-year strategy plan says.

Question 1: Can an agent reach your core banking ledger through a defined, authenticated, rate-limited interface?

Most NE Indiana cores expose a documented API surface, but the access pattern was designed for batch ETL, not interactive agent traffic. Pass band: a defined API, agent-specific credentials with scoped permissions, rate limits configured, and audit logging on every call. Partial band: API exists, but credentials are shared with batch ETL and there is no rate limiting. Fail band: no API; the agent would have to scrape an internal web app or read overnight ETL extracts.

Question 2: Is your KYC/AML data indexed, deduplicated, and accessible to an agent in regulator-readable form?

The unstructured-data problem the MIT TR piece names — 60 PDF variants for the same content — is the canonical NE Indiana KYC reality. Pass band: KYC/AML records normalized into a queryable data store, with audit-grade attribution back to source documents. Partial band: records are scanned and OCR'd, but the schema is inconsistent. Fail band: records live in nested folders by customer and year; an agent cannot find a 2019 SAR without a human searcher.

Question 3: Is your lending-decisioning workflow described deterministically?

The Mayzak determinism gap. Pass band: the lending workflow is documented as a deterministic decision tree with explicit rules, exceptions, and approval ladders — the description an agent can read and follow. Partial band: the workflow is described in policy documents but contains “officer judgment” language without bounded acceptance criteria. Fail band: the workflow lives in tribal knowledge; ask three lenders and you get three answers.

Question 4: Do you have a regulator-trace store for agent decisions?

Every action an FS agent takes against customer data has to be reproducible for an exam. Pass band: a tamper-evident store records the agent's prompt, retrieved data, decision, and the human-or-automated approver, with retention aligned to the FFIEC IT Examination Handbook retention guidance. Partial band: agent traces are kept but retention is unclear and the store is not tamper-evident. Fail band: no trace store; the agent's reasoning is unrecoverable.

Question 5: Is customer PII attribution traceable through the agent layer?

Every record an agent touches has to be traceable back to a named customer, a consent record, and a permitted-purpose. Pass band: PII is tagged at ingest, every agent retrieval is attributed to a permitted-purpose, and consent records are linkable to retrievals. Partial band: PII is tagged but permitted-purpose mapping is inconsistent. Fail band: PII flows through the agent without a permitted-purpose tag at all — the configuration most off-the-shelf agent platforms ship with by default.

Question 6: Where do your AI vendors' data residency, model-training, and breach-notification terms actually land?

The vendor data-handling layer is the surface that catches most NE Indiana FS firms by surprise. Pass band: every AI vendor has a signed DPA with US-only data residency, no-training-on-customer-data terms, and a 72-hour breach-notification clause aligned to the Indiana Attorney General consumer-protection guidance. Partial band: terms are inconsistent across vendors. Fail band: the agent platform's default terms permit training on customer data and there is no DPA in place.

A pass on six is rare for an institution running its first agentic pilot. A pass on four is a defensible launch posture. A pass on two or fewer means the audit work has to precede the pilot — running the agent against the current estate is a regulator-exam risk, not just a quality risk.

The 5-row FS Data-Readiness Matrix

The matrix below cross-references the five primary FS data domains against the four readiness dimensions every NE Indiana firm has to address before an agent touches production data.

| Data domain | Current human-query state | Agentic-AI required state | Regulatory-evidence requirement | NE Indiana mid-market typical gap |

|---|---|---|---|---|

| Core banking ledger | Batch ETL extracts; analyst-built SQL | Interactive API with scoped, audited agent credentials | FFIEC audit log retention; OCC model-risk traceability | API exists but credentials are shared; no rate limit; no per-agent log |

| KYC / AML | PDF and scanned documents in nested folders | Indexed, normalized, deduplicated, attribution-tagged store | BSA/AML record retention; CIP traceability; SAR reproducibility | 60+ PDF variants per content type; manual reconciliation; no deterministic schema |

| Lending decisioning | Policy document plus officer judgment | Deterministic decision tree with bounded exceptions and approval ladders | OCC model-risk explainability; ECOA disparate-impact testability | "Officer judgment" language; non-deterministic exception paths; no decision-tree representation |

| Customer 360 | Multi-system view with manual reconciliation | Unified entity store with consented permitted-purpose flags | Indiana DFI consumer-protection guidance; GLBA Safeguards Rule | Customer 360 project never completed; PII attribution flows are partial |

| Fraud monitoring | Rules engine plus analyst review | Continuous agent-monitored stream with regulator-trace store | BSA/AML reportable-event evidence; FinCEN reporting traceability | Rules engine outputs are auditable but agent overlay traces are missing |

The matrix is the working agenda for the audit. The first column names the data domain, the middle three columns set the bar, and the rightmost column is the gap every NE Indiana firm has to close before the corresponding agentic use case is regulator-defensible. The matrix is also the place to apply the NIST AI RMF — the four functions (Govern, Map, Measure, Manage) map cleanly onto the readiness columns, and the Conference of State Bank Supervisors AI guidance provides the community-bank-specific overlay.

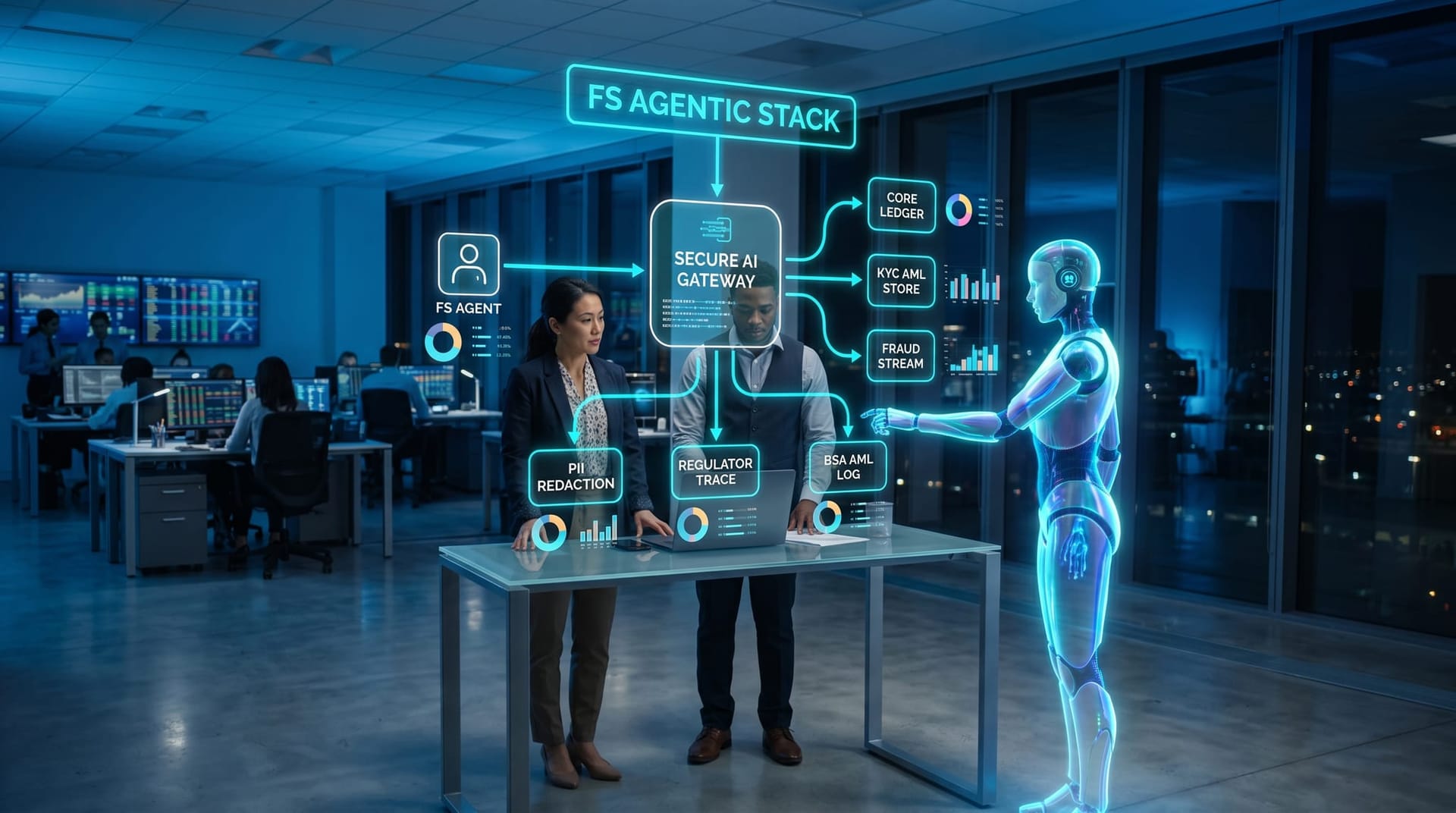

Where the Secure AI Gateway sits in an FS-regulated agentic stack

The architectural piece that makes the audit operational is the Secure AI Gateway. For FS work, the Gateway has to do four things that an off-the-shelf agent platform does not do by default.

First, PHI/PII redaction is server-side of the agent harness, never inside the agent. The agent never sees the un-redacted customer record; the Gateway intercepts the retrieval, redacts according to the permitted-purpose tag, and returns the redacted view. This is the only architecture that survives an FFIEC examiner's question about how PII is handled in the agent path.

Second, the regulator-trace store is hosted by the Gateway, not the agent. Every agent call writes a tamper-evident record (prompt, retrieved data, decision, approver) to a store the agent does not have write access to. The trace store is the artifact the BSA officer, the compliance officer, and the OCC examiner will read. The buyer-owned AI agent harness post covered the broader argument for buyer-owned persistent state; for FS, the regulator-trace store is the load-bearing version of that argument.

Third, BSA/AML reportable-event logging happens at the Gateway. When an agent identifies an unusual pattern that would trigger a human-officer review under existing BSA/AML rules, the Gateway logs it, routes it to the human review queue, and prevents the agent from independently disposing of it. The logging is server-side, the routing is governed, and the human-checkpoint is mandatory.

Fourth, agent identity, authorization, and approval-gate logic live at the Gateway. This is the Fort Wayne AI agent authorization audit layer applied to the FS context. Per-agent credentials, per-purpose authorization scopes, and configurable human-checkpoints for irreversible operations all sit in the Gateway. The agent platform vendor's identity model is supplementary, not authoritative.

The Gateway is not a single product; it is the architectural pattern Cloud Radix deploys for FS clients. The pattern is the only one I have seen survive both the technology decision and the eventual exam.

Four NE Indiana FS archetypes and the first data wall each one hits

Each NE Indiana FS archetype below is anonymized but composite — drawn from the conversations I have had with operators in the region this year.

Archetype A: A $1.2B-asset community bank in Allen County with three branches. The bank's first agentic use case is a deposit-operations agent that helps frontline staff resolve customer queries — balance inquiries, statement reissue, fee disputes. The data wall the bank hits is Question 1 of the audit: the core ledger's API is documented, but the credentials are shared with the nightly ETL extract and there are no rate limits. The first thirty days of the project are spent provisioning a scoped agent credential, configuring rate limits, and adding per-call audit logging. The agent does not touch production data until the credential and audit posture is in place — the Indiana Department of Financial Institutions examiner would not accept the alternative.

Archetype B: A community credit union in DeKalb County with $400M in assets and one branch. The credit union's first use case is a member-onboarding agent that ingests applications and routes KYC review. The wall is Question 2: the KYC document estate is a folder hierarchy by member and year, with no normalized schema across documents. The first sixty days are spent building an ingestion pipeline that normalizes documents into a deduplicated, attribution-tagged store — the same architecture the MIT TR piece describes Elastic and others building. Only after the pipeline is in place can the agent reach the data with deterministic results.

Archetype C: An independent property-and-casualty insurance brokerage in Fort Wayne, sixty employees, four producer teams. The brokerage's first use case is a claims-intake agent that captures first-notice-of-loss conversations and produces a structured claim record. The wall is Question 5: PII attribution. The brokerage's existing tooling lets staff paste claim narratives into vendor portals without a permitted-purpose tag — a shadow-AI risk surface squarely in scope of the Indiana AG consumer-protection guidance. The first ninety days are spent retiring the shadow-AI workflow, instituting a permitted-purpose tagging scheme, and routing the agent through the Gateway so the redaction posture is enforced.

Archetype D: A registered investment advisor in northern Allen County, $300M AUM, six advisors. The RIA's first use case is a meeting-prep agent that reads the client's portfolio, recent transactions, and advisor notes, then drafts a meeting agenda. The wall is Question 4: the regulator-trace store. SEC examination guidance and the OCC's broader model-risk posture both require that any AI-influenced advisor work product be reproducible — and the RIA's first instinct, to run the agent inside a vendor's platform without a buyer-owned trace store, fails the requirement. The first sixty days are spent standing up the trace store and configuring the agent to write to it.

Each archetype has a different first data wall. The audit's job is to identify the wall before the pilot launches, not after the regulator's exam letter arrives.

The 6-week NE Indiana FS Data-Readiness Audit pilot

Cloud Radix's six-week NE Indiana FS Data-Readiness Audit is designed for community banks, credit unions, insurance brokerages, and RIAs that have either started an agentic pilot and stalled on data, or are planning a pilot and want the audit done first. The deliverables are six artifacts: a scored data-readiness assessment against the six-question audit, a completed FS Data-Readiness Matrix for your five primary data domains, a Secure AI Gateway architecture sketch sized to your stack, a regulator-trace store specification aligned to your primary regulator (Indiana DFI, OCC, NCUA, SEC, or state insurance), a vendor data-handling review against the FFIEC IT Examination Handbook and NIST AI RMF, and a prioritized 90-day remediation plan with sizing for your team and your existing IT partners.

We anchor the audit work in NE Indiana's regulatory layer — the Indiana DFI, the Indiana AG consumer-protection division, and the Conference of State Bank Supervisors AI posture — and we work alongside your existing core vendor, IT MSP, and outside counsel. The audit is not a vendor-replacement engagement; it is the diagnostic that the rest of the program is built on. For adjacent regulated verticals — law firms and accountants in particular — the Fort Wayne compliance-automation post covers the parallel pattern.

If you are an NE Indiana FS operator with a stalled or planned agentic pilot, contact Cloud Radix to scope a six-week Data-Readiness Audit. The engagement starts with a ninety-minute scoping call and a non-disclosure agreement; everything we see is held under the confidentiality your auditors expect. The Cloud Radix AI consulting and Secure AI Gateway services are the two engagement paths after the audit, scoped against whichever data walls turn out to matter most for your institution.

Frequently Asked Questions

Q1.Why is data readiness specifically harder in financial services?

Financial services has a wider and deeper data estate than most other regulated industries, plus a heavier evidence-and-explainability requirement from regulators. Per MIT Technology Review's reporting, Forrester found that 57% of financial organizations are still developing the capabilities to leverage agentic AI, and a Gartner figure cited in the same article — that more than half of FS teams have implemented or plan to implement agentic AI — captures the gap between intent and readiness. The combined effect is high implementation intent, uneven production readiness, and a regulatory layer that does not give the institution the option to defer the readiness work.

Q2.Can a community bank or credit union actually pass the audit?

Yes, but rarely on a first pass. Most NE Indiana FS institutions score in the partial range on three or four of the six questions and in the fail range on one or two. The right working target is to pass on four out of six within ninety days of completing the audit — which is enough to defensibly launch a first agentic pilot on a bounded use case. Passing on six is a multi-quarter program for most institutions.

Q3.What is the relationship between the Secure AI Gateway and our existing core banking system?

The Gateway sits in front of the core, not in place of it. The core remains the system of record; the Gateway is the access boundary the agent talks to, with redaction, audit logging, regulator-trace store, and authorization scoped per-purpose. The core vendor relationship does not change. What changes is that the agent never gets a direct connection to the core — every call passes through the Gateway, which is the architectural posture that lets the institution answer an examiner's question about agent access cleanly.

Q4.Where does Indiana state regulation fit relative to federal?

The federal regulators (OCC for national banks, FDIC and Federal Reserve for state-chartered banks, NCUA for federal credit unions) set the primary safety-and-soundness expectations. The Indiana Department of Financial Institutions adds state-chartered-bank and consumer-finance oversight, and the Indiana AG's consumer-protection division adds the state breach-notification and consumer-protection layer. For most NE Indiana community banks and credit unions, the audit has to be passable under both the federal and state lenses simultaneously — and the regulator-trace store and PII attribution posture are the load-bearing artifacts for both.

Q5.How does this differ from the agent identity and authorization work?

The two are complementary. Data readiness is about whether the agent can reach the data in a reproducible, auditable, regulator-defensible way. Agent identity and authorization is about which agent reaches the data, with what credentials, scoped to what permitted-purpose. The data-readiness audit usually precedes the authorization audit by a few weeks, but both have to be in place before a regulator-defensible pilot launches.

Q6.What does the six-week audit actually look like in practice?

Week one is scoping, NDA, and a kickoff session with your CIO/CTO and BSA/compliance officer. Weeks two and three are interviews with line-of-business owners and a technical review of the data stack. Week four is the regulatory mapping — aligning the readiness gaps to NIST AI RMF, FFIEC, OCC, Indiana DFI, and your primary regulator's specific guidance. Week five is the Gateway architecture sketch and the trace-store specification. Week six is the deliverable review and the 90-day remediation plan with your team. The audit is engineered to be done while your core operations continue uninterrupted.

Q7.Can we run a small pilot first and do the audit afterward?

It is possible but inadvisable. The risk profile of running an agent against production FS data without the data-readiness audit and the Gateway architecture in place is materially worse than the cost of doing the audit first. The audit is sized to be the cheapest and fastest step in the program. Most stalled NE Indiana FS pilots stalled because the audit work was skipped — running the audit first is the path that ships a defensible production agent fastest.

Sources & Further Reading

- MIT Technology Review: technologyreview.com/2026/05/14/data-readiness-for-agentic-ai-in-financial-services — Data readiness for agentic AI in financial services.

- NIST: nist.gov/itl/ai-risk-management-framework — The AI Risk Management Framework, the federal reference for AI governance.

- FFIEC: ithandbook.ffiec.gov — FFIEC IT Examination Handbook, the federal exam reference for FS technology controls.

- OCC: occ.treas.gov — OCC Comptroller's Handbook and AI guidance for national banks.

- Indiana Department of Financial Institutions: in.gov/dfi — State-chartered bank, credit union, and consumer-finance regulator.

- Indiana Attorney General: in.gov/attorneygeneral/consumer-protection-division — Consumer protection division, including breach notification and consumer-protection enforcement.

- Conference of State Bank Supervisors: csbs.org — CSBS AI guidance and community-bank-specific posture documents.

Scope a 6-Week FS Data-Readiness Audit

We will run the six-question audit against your community bank, credit union, insurance brokerage, or RIA, sketch the Secure AI Gateway architecture for your stack, and put a prioritized 90-day remediation plan on your desk.

Schedule a Free ConsultationNDA on the first call. We work alongside your existing core vendor, IT MSP, and outside counsel.